The Coolest Film Brand in the World

A Contrarian Bet on Originality

Godard said that the best way to review a film is to make a film and I think that the best way to criticize an industry is to start a company. I have an idea. It’s a new streamer that brings together much of what I have been saying. Let me know what you think. Anything new in streaming is contrarian because people think it is a crowded space. But I think there is a big gap in the market and in our culture. If there are many restaurants in town but they are all vegetarian, is the market crowded or is there a gap? I say gap.

Key observations:

Indie film is spread thinly across the various streamers. It has no brand or home, which dilutes the energy of the space.

Hollywood is backing away from prestige TV

Hollywood has pulled back on comedy

So the idea is to consolidate the indie film space through acquisitions and launch a streamer that is the one clear leader and place to go if you are into smart, interesting film. In TV, supplement selection by producing the prestige TV and comedy that Hollywood doesn’t seem to want to make anymore.

We are not going to push Netflix into the sea, but we will create the coolest film brand in the world and there will be an audience for that.

I am going to argue that this is possible and would be good economically and culturally.

A basic premise about the streaming sector: there are everything stores and there are boutiques. Boutiques are selling you a specific thing, like Major League Baseball, Disney, Mubi, Crunchyroll, or Britbox. I am pitching you a boutique. But if we make it cool and fun I think it can be a big boutique, like 20MM to 25MM US subscribers, smaller than the old HBO but bigger than Crunchyroll or Mubi.

“Indie” or “prestige” films are original and distinctive films that often appear in festivals and often contend for and win awards. By indie I don’t mean that they are literally independently financed or that they are obscure or small. I mostly just mean that they are original and interesting and smart, so I include everything from Pulp Fiction to Falling Leaves to The Holdovers to Everything Everywhere and I would argue for Oppenheimer at least to be called “prestige” if not indie.

There is an indie streamer, called Mubi, and in the past FilmStruck (part of Turner Classic Movies, I believe) and Fandor both gave it a shot. Criterion has had a service, though it is just the licensed Criterion library. These are and were all too small. The idea has never been executed at scale.

Programming

Film

With some modifications to be discussed below, this needs to be my screen if I load up the app today (except we would also have original series):

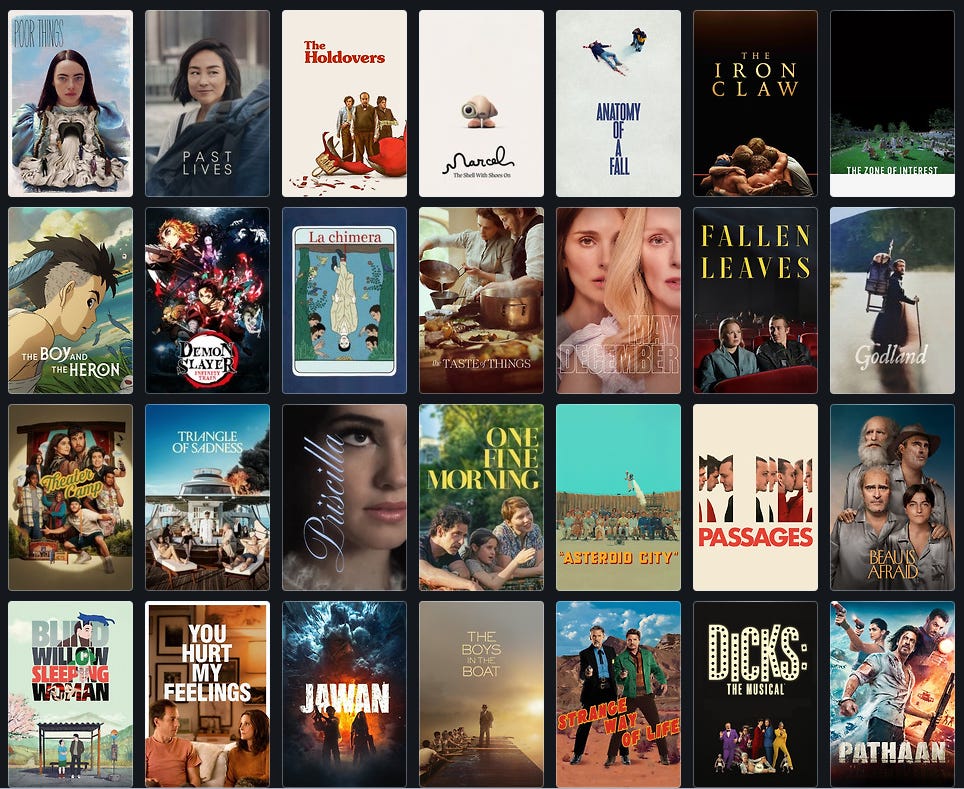

This list of 28 movies from the past year or so includes most of the prominent indie-ish or foreign films that got the most attention.1 The service has to have just about everything in our zone. I did leave out some things, allowing for realistic competition, including Ferrari and Maestro and particularly the super expensive films like Killers of the Flower Moon and Oppenheimer. But in the future or theoretical universe where this company exists, we outdid competitors for the Alexander Payne film, the Yorgos Lanthimos, the Nicole Holofcener, the Sofia Coppolla and the Wes Anderson pictures and we landed Godland, American Fiction and The Taste of Things. So you’ve got five pictures in competition in Cannes and about three Best Picture noms. To accomplish all of that, it means that you must have cash and an A team that knows festivals, is the best in the business at film releasing, and who do a great job with awards promotion. Do you actually have to beat everyone on all 28 of these films? Not every single one, but this will work much better if you are the clear leader in the space.

In addition, one would need:

A robust library with everything from Spring Breakers to Il Sorpasso to In the Mood for Love to Moonlight and, finally,

12-18 original series in the US

But I want to turn up the heat here as I look at this list of 28 films. I have been imploring the indie world to expand the audience by delivering more energy and fun. You may recall my criticism of the nostalgic feeling of Cannes. We do not want that. We want to always do the daring thing. I enjoyed Fallen Leaves and we can have those movies, but we can’t have too many titles getting $0MM to $5MM at the box office. Culture needs to evolve with the audience and what I need in this mix is a bit more of What We Do in the Shadows, Spring Breakers, Baby Driver, Sexy Beast, Pulp Fiction, Get Out, Everything Everywhere All at Once, i.e. fun, kinetic, comedic, originals and some elevated genre. We must build the dangerous, transgressive and lively culture brand of tomorrow. So – edge, some genre elements, and energy. There is a gap in the market now for fun films and we would miss an opportunity not to grab that. Is that a different audience from our core indie films? I don’t think so. If comedy is not allowed in Hollywood and this is the more edgy, art brand, the Ramones of film, the Wu Tang Clan of film, then of course we will do comedy.

Television

At the same time, is Hollywood not giving us a major opportunity in television almost begging someone new to enter the market? There is a certain kind of show that built premium cable and built streaming – “prestige TV” – that the streamers are leaving behind. I discussed this here in a New York Times piece. Many of what might be your favorite shows, or what might be regarded as the best shows of all time, such as The Sopranos, The Shield, Breaking Bad, The Wire, Veep. Curb Your Enthusiasm, The Larry Sanders Show, Mad Men, etc. would not be made today and I would note that shows like Yellowstone, Billions, Marvelous Mrs. Maisel, The Crown, The Boys and Succession were all developed and ordered before the change that occurred around 2017. The change has something to do with seeking broader audiences and it also has to do with avoiding shows that feel too elite or are too hard to write. (Or that have comedy.) Occasionally, a show sneaks through that would have fit in in the previous era, like The Bear or White Lotus, but rarely. We see the impact of this policy change in the decline in 8+ IMDb ratings of new series over the years (except at HBO):

Netflix was down 75%. They really did a 180 after they parted ways with Cindy Holland.

Amazon was down 56%. Also arguably personnel related (!).

Whatever afflicted those streamers did not affect HBO, which did not drop off at all:

In the last four years, the audience received 35 fewer 8+ series than it did in the four years 2014-2017, a decline of 43% (this despite producing more series overall). Consider that an engraved invitation. Churn is up across streamers in 2023 and this must be one major reason why.

I won’t go into the decline of comedy in as much detail but suffice to say that comedy used to capture 15% to 20% of the box office every year and in recent years it has sunk to ~5% with the exception of 2023 because of Barbie, which is an outlier. Hollywood just doesn’t want to make The Hangover or Tropic Thunder anymore, which is an opportunity.

I do not think that any of these changes have been driven by market forces. America still loves to laugh and they would still value fascinating character-driven series. I know that the writers who can write this material are out there ready to create the next great series, often with pilot scripts on their laptops. Let’s make those shows.

By the way, for context, my personal average IMDb rating per season of television, across all seasons, is 8.1. We can do this!

Bottom line. You want your brand to wind up in that Supreme/A24 zone where your fans are wearing the t-shirt.

You want the coolest film brand in the world. Not the one with the most dragons. The next SST Records. The next Def Jam Records. The one with the most posters on dorm room walls.

Other Engagement

If you want to grow an app and hang on to customers, you need frequent engagement. How do we get customers engaging with the app daily or weekly? Most basically, through the content. But we also want to experiment with content formats that are 52 weeks per year that generate shareable shorts (think: our SNL) and with community features that increase engagement ala Discord. I want users to regard the community as something like a club with fresh content every day. Too many SVOD services feel like a museum.

This could include interesting podcasts and docs about culture and the history of film. Robert Edwards and Thomas Flight are good examples of people who could be part of the brand.

One more adventurous idea I like as a driver of user visit frequency is the idea of acquiring, if possible, Patreon. You might think it would clutter the experience, but I think Spotify has handled incorporating podcasts just fine and I like the idea of a flow of high velocity content that drives frequent app opens.

There has been very little innovation at media companies in terms of community features (or any features) in their widely distributed apps. We should try to do better.

How to Begin

This cannot start from scratch. You have to consolidate the space. All companies are always for sale but some are more for sale than others. There is only one way to find out.

A24: The leader in the space. A good place to start.

Neon: Someone at Neon definitely knows what they are doing. They had Parasite. They have Anatomy of a Fall. They always pick the winner at Cannes. This is a good start but has to scale up and get a bit more commercial.

Mubi: Not essential but, suffice to say, at the right price it’s helpful.

Miramax, Spyglass, Criterion: helpful libraries with some development.

GKids: They get a lot of top Asian films including Studio Ghibli

Landmark Theaters: Landmark has a lot of important indie theaters. They even have a mini-streaming service. Could be a helpful asset (not essential).

Longshot: Searchlight: Disney should absolutely sell Searchlight which has no overlap with the Disney or Hulu brand or audience. Will they? Maybe not. No one has said anything about it, so probably not. But you never know. I mean. I think they clearly should.

Patreon: As discussed.

To this mix, one would have to add some incremental capital to ramp up output to the level desired by the service as a whole.

Does this work at scale?

I will just do this at a high level. Here are a couple of original TV content budgets to create a range:

For the films, assume that you have a pay two output deal with, say, Netflix, and a FAST deal, and you distribute to theaters, PVOD, TVOD, AVOD, and physical media. You license foreign rights outbound. So your net exposure to the 28 original films per year is the pay one window and let’s say that this averages $8MM per film so your net negative on this program is $224MM. I am going to say you pump that up to $250MM with some pick ups, maybe a few docs. Your gross investment in that set of films by the way, assuming they average $12MM in production costs, is $336MM plus marketing which will about double it to $672MM. But your net exposure is $224MM.

We said we would have a robust library so let’s throw half a billion into that every year (not amazing but given that we have a narrow category probably acceptable).

So the aggregate net content investment per year is $500MM + $224MM + $466MM = $1,190MM. Your P&L will make it look like your investment is larger – it is – but you are offsetting it. This is the net negative cash. Not a huge service by any means but carefully curated.

On top of your content investment, you have marketing and general and administrative costs. For these I am just going to pull numbers directly from Lionsgate’s 2023 Annual Report for their Media Networks segment which is Starz, which is a good comp. That would give us $496MM in Distribution and Marketing Expenses and $100MM in General and Administrative Expenses.

So all in all, the cost side looks like:

Content $1,190

Marketing $ 496

G&A $ 100

Total $1,786

Here are two revenue scenarios. In the first, we have 25MM subscribers at $12 per month and 80% of them subscribe directly, not through any discounted bundle or through Amazon Channels. In the second, we have 20MM subscribers at $10 per month and only 60% subscribe directly. In the first scenario, we have revenue of $3.3B and in the second $2.0B. Note that in reality, you would also have AVOD, PVOD and TVOD revenue streams, which I have left put but which would be additive to the economics.

In scenario one, we have $1.5B in EBITDA. In scenario two, we have $230MM of EBITDA.

Why would this service have 25MM subs when Starz has about 20MM subs and why is our ARPU twice Starz’s? I would argue that the service presented here would have three Best Picture nominees per year and multiple Best Series Emmy and Globe nominees. It would get a ton of free, what they call “earned,” media. Many people would think of it as their favorite service and their favorite show or film would be on the service. It is a premium service that, if everything is executed as planned, will punch above its weight. None of that is true of Starz, Mubi or even Paramount+. Why do we think Paramount has a low ARPU (~$6)? Because it has no brand or identity. South Park is licensed to Max. Yellowstone is licensed to Peacock. The Star Trek movies are licensed to Max. There is no there there. Mubi has 12MM members worldwide at $12.99 and the service I am describing has much more customer appeal than Mubi. On the TV side, the service described would have a good shot at the next White Lotus or Succession. Starz doesn’t have that. Mubi doesn’t have TV at all. I think these services are in different categories and would get different results.

My expectation is that scenario one ($1.5B of EBITDA) is a more realistic outcome than scenario two for the proposed service. If the company value is 13X EBITDA, then in that case our value is $19.8B.

If the terminal value is in the neighborhood of $20B this is all definitely worthwhile economically. I think it is beneficial culturally because it would create a strong economic foundation for the future of our most interesting films and television shows.

FAQ

Why only in the US?

Think of foreign as v2 optionality. You could make lighting up all 190 global countries and territories a p0 launch blocker, but it will significantly delay launch and do you really want to delay launch for that? It will be better to get into the market.

There is another version of this where you bring on Waave (SK Telecom), TVing (CJ ENM), Hulu Japan (NipponTV), Canal+ (Vivendi), and/or Hotstar (Reliance) as partners and/or strategic financiers from day one and you have a robust international footprint from the start. That could work.

A complex decision here is what properties you want to keep global rights for in anticipation of a global launch. You do not want to have to go around and buy rights back later. But if you retain a lot of foreign rights, your production negatives will obviously increase.

What is the best counter-argument?

The best counter-argument is that the competition in the indie segment would be a real knife fight and you just would not be able to secure a very, very strong king of the hill position. Focus or A24 or Searchlight are not just going to go away. I am not that worried about this. The premise is that we are consolidating one or two of those competitors and our slate is differentiated in multiple ways.

Where could the model most likely be wrong?

We could decide to hang on to foreign rights to original series, anticipating overseas expansion. This would increase annual original series net investment by ~$200MM.

Starz runs a very tight ship. Using their marketing and G&A may turn out to be incorrect and we may wind up surpassing that by ~$100MM.

Neither of these changes changes the answer.

What about competing with Netflix?

This product is pretty different from Netflix or any other major service. Many of our subs would have both services. But I think this service would have one of the clearest unique selling propositions in the industry. That doesn’t mean it would appeal to everyone. But it would be clearly differentiated and it is not like any other service. It is probably most like HBO but at this point HBO is buried deep within MAX.

What are the most important early steps?

Get the right team.

Get the financial partner.

Close the mergers.

Go

Roy Price was an executive at Amazon.com for 13 years, where he founded Amazon Video and Studios. He developed 16 patented technologies. His shows have won 14 Best Series Emmys and Globes. He was formerly at McKinsey & Co. and The Walt Disney Co. He graduated from Harvard College in 1989.

I realize now that I should remove Triangle of Sadness and put in American Fiction because Triangle was from 2022. Oops. But you get the idea.

I dig it. Great post. I hope the right folks read this.

I think the other things that streaming so far has neglected -- and that most companies have also neglected -- are attitude, context, authenticity, engagement, takeaway, & community. These are all critical aspects of cinema that get lost in the focus on transaction, convenience, and access. If you want to play to win and play to last, they have to be in mix. But that can be done. To me what you are pitching is not "indie" or "presitge", but "CINEMA" or maybe "CINEMA, DAMNIT!"

As always Roy a thought provoking and enjoyable read. Rob long also commented on, if you like the “fear of comedy” and as I suggested to him there is an elephant in the room that everyone skirts around as you to have also done so masterfully here, why indeed no more Hangover or Tropic Thunder? just the feminist juggernaut Barbie. As I’m a intellectual lightweight I leave that up to you heavyweights to ponder while I’ll join the great un washed masses watching Ricky Gervais and Dave Chappell on Netflix both hitting number 1 in my my country in the last two weeks.