How to Build a New Era in Hollywood

The Day After the Day of the Locust

Compared to today’s Hollywood, The Day of the Locust was quite upbeat.

Warner Bros. Discovery wrote down $9 billion of their cable networks’ book value. Paramount did the same for $5 billion and laid off 2,600 people. Not a week seems to go by without more layoffs. The Wrap is doing a whole series on how blue everyone is.

At least Twisters and Deadpool did well. Hollywood in general seems to be learning a lesson that I have been pushing for quite a while — focus on entertainment, not politics, and try to serve all the people. 2018-2024 was a fad and that fad is over.

Let’s take a look at a couple of players and then at the state of getting individual movies made.

But first, let me start with my basic point of view about SVOD services.

Let’s say this is Netflix.

Then your service can’t be this.

Who goes to 13 Flavors? Not many people (unless your 13 flavors are very specific).

What if 13 Flavors cut costs so that it could make a small amount of money on its limited revenue? Well, okay. Here is the choice you have. Here is what quarterly cash flows should look like for a subscription video (SVOD) service over time.

If you get down to -10 and it is all too painful, though, and your board is freaking out, the press is asking questions and your oldest daughter says that the girls at Marlborough are teasing her about your quarterly earnings per share miss, you can always take the chicken exit. You can cut costs way back and you can wind up with a chart that winds up like this.

The only problem is that while you have avoided the pain of the final climb, you have also failed to make the total investment required to have a world class service that earns meaningful returns.

You are the guy on the bottom:

I feel like that describes a few players in Hollywood today.

Disney

Disney stock is at $86.16 as I write this (-3% for one year and -56% vs its 2021 peak). Let’s compare some numbers with Netflix.

Netflix subscribers: 277 million

Disney subscribers: 205 million (Disney+ 118, Hotstar 36, and Hulu 51)

Netflix revenue: $9.6 billion

Disney streaming revenue: $6.4 billion (67% of Netflix)

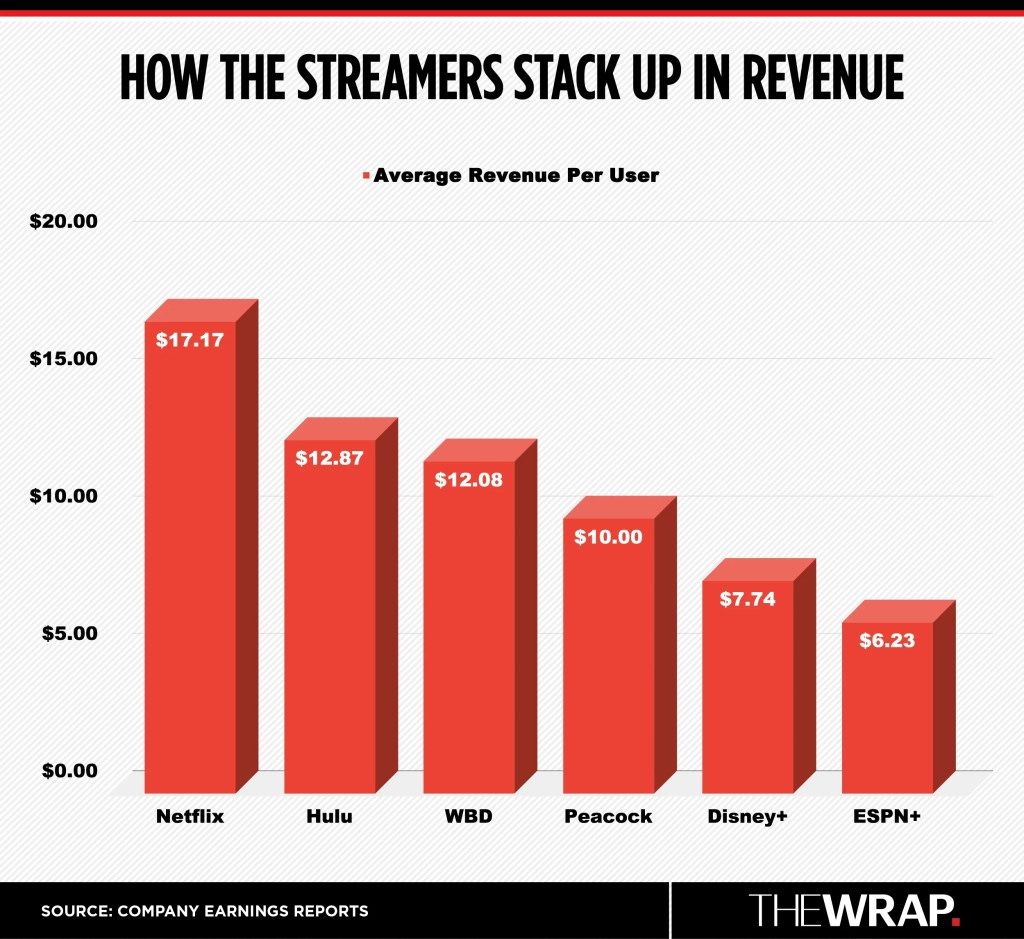

Netflix monthly revenue per customer: $17.17 (US-Canada), $10.80 (EMEA), $8.28 (Latin America), $7.17 (Asia Pacific).

Disney revenue per customer: $7.74 (domestic, -3% q/q), $6.78 (international ex-India, +2% q/q), $1.05 (India, +50% q/q)

Here is the whole industry by domestic ARPU —

It seems possible that the Disney subscriber base will not grow a lot from here. Usually, you don’t grow and grow and then go flat and then suddenly start growing rapidly again without some transformative product change. So how do they go from where they are financially — essentially break even — to making meaningful money in subscription video? Well, if Disney+ charged $17.17 per month (like Netflix) to their 54.8MM US subscribers, they would bring in an extra $6.2B per year. Their business would then look (obviously) much more like Netflix’s.

The fact that Disney’s domestic ARPU was down this past quarter and subscribers were barely up is troubling. The question on Buena Vista St. really has to be — how can we raise prices without losing subscribers? But if their customer base is price sensitive at this level, that poses a serious challenge. It means they need to increase value.

It is hard not to suspect that the price/growth dynamics here have to do with Disney’s recent inconsistent creative. Disney’s announcements coming out of D23 did sound promising, with new projects coming from top talent. Disney has a Royal Flush of IP. It’s hard not to win. But they went through a recent period where they were making the least of it.

Is Deadpool a turning of the tide or just an echo from an earlier era? The selection of the next CEO will be critical.

Apple

Just briefly I will say that I do not entirely understand Apple’s strategy and I am not sure anyone else does either. When we started at Amazon and focused on prestige or when HBO was more or less inventing “prestige TV,” we both had modest target audiences and smaller budgets. Those strategies made sense in those circumstances.

In 2024, however, Apple and subscription video are mass market. It seems clear that they don’t have enough content and their tone is a bit too refined to drive mass adoption and frequent use. Jason Kilar was saying the other day on “X” that SVODs needed to set the goal of two hours of viewing per day per customer to get adequate customer retention and growth. While I do not think that 30 days and 60 hours per month is a hard requirement, there is no question that engagement drives retention and you want customers to engage multiple times per week to keep their loyalty. Apple just is not programmed for that.

To be clear, I have enjoyed some of their shows, but to move the needle they need more content and they need to be broader. Their movie strategy in particular has focused on very expensive high prestige (in theory) films that haven’t really worked out. Usually these have big stars and legendary directors, e.g. Killers of the Flower Moon with Leo and Scorsese. Matthew Belloni had a good podcast on this issue recently. That is not working. They need more content.

Many journalists have fantasized about Apple buying a Hollywood studio. Despite their need for more volume, I personally think this is unlikely. If you’re Tim Cook and you have an organization working quite well that you understand, do you want to divert part of your day thinking about showbiz and perhaps theme parks? I doubt it. Licensing seems more likely.

Warner Bros.

Warner Discovery stock has crossed the Mocha Cookie Crumble Frappuccino line at $6.94 (-50% over one year).

Last quarter the Warner Bros. studio made (EBITDA) $200MM, their TV networks made $2B, and streaming lost $107MM. So TV provides 95% of the cash flow.

The problem (which is also the problem at Paramount and NBCU), is that the TV cash cow is rapidly declining and the movie part is not likely to grow very much. So if the company is going to grow as a whole at all, or shrink more slowly, it’s all up to the streaming service. (By the way, their global ARPU is $8 and their domestic ARPU is $12.08.) Warners is really the perfect model for the miner meme above.

The service has a strong team and some marquee properties on the way, including a Harry Potter series and more Game of Thrones. However, as I have said before, they need way more stuff. I’m sure there is a more eloquent way to say that, but basically, they do. I have thought that they need about another billion dollars of original content and I still think that is true. I realize this is a random week but I find this table a bit disconcerting. No Max.

Step one: take $1B from next year’s operating plan and invest further in streaming so that it can gain value.

Sadly, I love Warner Bros. and HBO but this whole thing just kind of hasn’t worked. It seems obvious that Max and WBD haven’t lived up to the projections in whatever spreadsheet drove the Warner Bros. acquisition. Why does WBD stock go down when they have an earnings release? Because what people need to see is that the streaming leg of their business stool is going to be a big success and make up for the gradual decline of TV. But that’s not what we see in the numbers. It is not evident that they are trying to get big. It looks like they are trying not to lose. You need to be getting to 31 flavors. If you are sort of maintaining a flat position, the whole thing looks pointless and its future value, which in some spreadsheets might have had a $100B terminal value against it, just declines to somewhere around zero.

A merger could help.

Paramount

The tripartite leadership at Paramount seems to be following through on the Shari Redstone era plan of cutting costs and jobs on their way to profitability. They announced a cut yesterday of 15% of employees, including the deletion of all of Paramount Television. Ouch. I hope that they have conferred with David Ellison and Jeff Shell.

Personally, I have real concerns about this approach as it smells of the “we’re going to cut costs until we break even” strategy when what is needed is growth.

One option for Paramount would be to commit to a differentiated and branded creative strategy building on Yellowstone and CBS, as discussed here. They could do this and succeed without any mergers.

Barring that, it could also work for Warner Bros. and Paramount to merge and offer 32 Flavors. I think Zaslav agrees with this (he met with Paramount to discuss). Both services need to bring more to customers, so a combination could make sense.

Either way, I have high hopes for the incoming team.

As a final thought on the studios and services, I will just mention that, as I have discussed before, if people cannot get over the hill themselves and they cannot merge, then the optimal outcome is for studios to aggregate their content on a shared, open, global streamer to come into existence where all of the transactions and economics are transparent and equitable. This would be like BitTorrent but with a business model and would be built on crypto rails. I think this is ultimately going to exist and would benefit many in Hollywood as discussed here.

Players Matter

Zooming out, sometimes the problem is the players on the field and this has been a recurring, if implicit, theme in these analyses. I do not see a lot of innovation and there are many people who seem to like the strategy of either getting out of streaming or just cutting costs so you don’t lose money. Not a great idea. What are you left with? A dying TV business and a no growth studio? That’s nostalgia and would have a p/e of about 3.

I really think many of these people are just … from the cable/DVD/smoking in restaurants era, which is not helpful. You need the best team for today.

Another issue is that I think there was this notion for a while that “hey, anyone can do this.” And so we did a little experiment and let a lot of JV players start. It was really a weird jubilee that one day people will write about. Do you think it worked? For whom? Let me ask you this — who are the next wave of CEOs around Hollywood who are super impressive and ready to take on today’s challenges but aren’t currently CEOs? Can’t think of any great candidates? Doesn’t that seem unusual for an industry?

But what about your movie?

But what about your movie? What category of movie is looking promising today?

What do people want? What can get made? Let’s look at 2023. I know — a bit of a lame year, but 2021-2022 are weird years, this is a weird year too, and we can’t go into the future, except in real time.

If we look at the 2023 top 100 films by US Box Office, number 100 comes in at $10.5MM. The top 100 as a whole account for 95% of the box office for the year and you don’t really want to come in under $10 because then you’re going to be unprofitable at a budget of $8MM and everything below that is just … a slippery slope. The exception of course is if you are doing a European production where you have European subsidies and revenue and you really don’t need US money such that if you get zero for theatrical and $3MM for streaming it’s all gravy and it’s fine. If that’s your situation, you do not have to gross $10MM in the U.S. I mean, would I do the next Pawel Pawelowski or Aki Kaurismaki movie? For sure.

But if we assume you’re not doing that, then your goal is to be on this list of the top 100. The list is mainly major IP and sequels. The first non-IP non-sequel is #10, Sound of Freedom, which is interesting but a bit of a fluke. After that, it’s M3gan at #26 with a $95MM US gross (didn’t do well overseas). Cocaine Bear is at #40 with $64MM (bombed overseas). The Boys in the Boat is #48 at $52MM. The first real “indie” indie is Poor Things at #61 at $34MM. American Fiction grossed $21MM. The Holdovers got $20MM.

I’m including everything that is an original film and not a studio assignment on a franchise, which totals to about 33 movies. If we exclude horror films, we are left with a couple comedies (Anyone But You, Cocaine Bear) and indie dramas (American Fiction, Poor Things, Holdovers). Note, the Palme d’Or winner, Anatomy of a Fall, did not make the list so … there you go.

I think these break into two categories, the commercial film and the prestige film.

A lot of the top films here — Cocaine Bear, Anything But You — are big packages in the $25MM to $35MM zone. If you have Glen Powell and Sidney Sweeney (in 2023) in a commercial picture for $25MM, absolutely go for it (I fear those days are done though now that they are huge stars). Note, as fun as it was, I suspect Cocaine Bear did not make money. It grossed $25MM overseas, less than half its domestic gross, which is far less than you want it to be. So that $35MM mark can be risky. So I like this $25MM zone.

But I will not pretend that Civil War does not exist even though it is not in our 2023 dataset. That is a big unconventional action film at $50MM. Big genre, bold, with a name and a great director. Makes sense for an action film.

Poor Things, clearly a prestige film, had a quirky premise but big auspices. At $35MM it grossed $34MM in the US. So, normally not a winner. But the foreign was $77MM, which gets it over the top. Personally, again, this $35MM zone can be tough. I think this would be a bit out of my zone if I were setting rules, but on the other hand it would be hard to pass on this one. That’s showbiz, folks!

If you have a genre element and a more prestige name and a filmmaker, your more comfortable prestige budget zone is usually going to be more like $5MM to $15MM for your Holdovers and American Fictions. The Everything Everywhere budget was $14MM (so was Jojo Rabbit) and it had a lot of action so you should be able to do your thing for that or less.

So those are the two zones. That’s the lay of the land. There were 27 slots that were not horror or foreign or huge movies like Killers of the Flower Moon. The key obviously is to get the right package for the material, because remember that in pitches or financing meetings, your odds are either 90% or 2%. They are rarely 50%. That is, you either have Greta Gerwig, Yorgos Lanthimos or Alex Garland and Emma Stone or Austin Butler or you don’t.

But as a final thought, stepping back, I would add that you can’t really reverse engineer success. I am not over the moon with this list of films and I think what the market could really use is a truly new era and a bit more of an adventurous and artistic few years.

What if we just launched into a future where everyone does the daring thing? That feels like a much better answer to break out of the doldrums. Instead of trying to figure out what success looks like by looking backwards at, of all things, 2023, we should be looking forward and figuring out what will be amazing in two years.

One thing you do not see looking backwards is that I think there is about $800MM to $1B of box office (10% of total box office) being left on the table now in the form of truly hilarious comedies that are not getting made (just because the percent of box office used to be 15% to 20% and now it is about 5%). That’s an opportunity because people, I believe, still love to laugh and comedy goes in cycles.1

And beyond that, great films don’t fit a mold. Creating a new future is where the future is. Being original is the best way to wind up with an amazing package.

The audience isn't dead. They're just bored. They're scrolling through Reddit and TikTok, hungry for something that doesn't feel like it was focus-grouped within an inch of its life. They want something surprising, a little outrageous, and impossible to explain to your parents.

We need the cinematic equivalent of Picasso's "Les Demoiselles d'Avignon" – something that makes you do a double-take and say, "What the hell am I looking at?" before realizing it's changed everything.

The audience is waiting.

Roy Price was an executive at Amazon.com for 13 years, where he founded Amazon Video and Studios. He developed 16 patented technologies. His shows have won 14 Best Series Emmys and Globes. He was formerly at McKinsey & Co. and The Walt Disney Co. He graduated from Harvard College in 1989.

For example, in 1972, there were only two comedies in the top 20 — What’s Up, Doc? and Everything You Wanted to Know About Sex. In 1974, Blazing Saddles was #1 and The Bride of Frankenstein was #4. By 1978, Animal House was #2 and 10 of the top 20 were comedies. So it varies.

Excellent as always, and it seems as though people managing studios are genuinely not talking to their consumers to understand what they actually want.

I don't mean letting fans pick movies, I mean fully understanding how Online, Multichannel, FAST and SVOD suit consumer's entertainment needs. TikTok filled a hole people didn't know they had (mobile, but shorter than Quibi) and took a lot of wind out of YouTube's sails. And YouTube is taking a major fraction of video watched on Televisions, not just laptops and phones.

The first studio that comes up with a big-picture, comprehensive view of what consumers want and need in total from their entertainment providers will have a big advantage because they will know where to play. The fact that Paramount-CBS has not embraced its massive advantage in Red America is professional malpractice.

There seems to be an absence of strategy here from almost everyone, just endlessly replaying the last few years while they wait for cable to die. If only there were professional service firms set up to help people figure out strategy....

(A note on your footnote. I think the 1974 film you're looking for is the sublime Young Frankenstein.)

As always a great read but more importantly ideas and a way forward, Roy you write consistently about the problems across the board and often provide what I think are commercial, fresh solutions and I echo Adrian Blake’s insightful comments below but is the real problem that they ( studio heads etc,) subscribe to your type of thinking but the political environment stops them from pivoting?